The Impossible Predicament of the Uninsured

· The Atlantic

The day after Thanksgiving, I got a voicemail. A woman identified herself as a doctor at the University of Louisville hospital: “I believe I may have one of your family members here.”

Visit asg-reflektory.pl for more information.

The message was hard to understand. Most of my family lives in Kentucky, so I didn’t know whom the doctor was referring to. I called the hospital, but kept getting put on hold. Then I tried my aunt—if someone was in trouble, she’d be the one to know. But she didn’t answer.

A few hours later, her son got in touch with me. My aunt was the one in the hospital. She’d had an aneurysm on the right side of her brain, and it had burst. The drainage tube the doctors used to stop the bleeding kept slipping loose; after three tries, they finally got it to stick. Only then could they do surgery. My cousin FaceTimed me afterward, from the ICU. “Are you ready?” he asked. He angled the camera down to my aunt’s face, and I started sobbing like a sudden rainstorm.

A few days later, I got on a plane from Washington, D.C., to Kentucky and went straight to join my family at the hospital. We had always called my aunt “The Glamourina.” She wore feathered hats with sparkly shirts and experimented with different hairstyles: a butterscotch-blond cropped cut, an afro, a bob streaked with highlights. She paid for my first real manicure, when I was in high school. We wore matching striped shirts to the salon, and used an eyeliner pencil to draw fake moles above our lips, like Marilyn Monroe.

She is 58 now, and raised two kids as a single mother. She always treated me like one of her children, and I grew up to look more like her than like my own mom. When I’d talked with her the week before she ended up in the hospital, she’d asked me to play our favorite song, “I’m So Proud of You,” by Julie Anne Vargas. Now the top half of her head was shaved and staples ran in a ladder across it. IVs were taped to each arm, and a machine next to her bed was helping her breathe. She couldn’t speak. When she opened her eyes, they rolled.

Her older son was especially alarmed by how quickly she’d declined. He wanted the doctors to come into her room so they could explain what had happened. But one of our older relatives stopped him, saying that we couldn’t afford to make demands, let alone trouble, because “she don’t have a lick of health insurance.”

We knew that the hospital couldn’t deny her care, but we understood the tightrope you walk when you don’t have money. All she could afford to be was grateful.

We don’t know what caused my aunt’s aneurysm, but she’d had persistent headaches for months, and she’d been worried. Once, when she was driving, the left side of her body turned numb and her toes curled up. She pulled over but didn’t go to the hospital; she couldn’t afford it.

My aunt worked as a hair stylist at a salon for years. Most recently, she was the overnight caregiver for an elderly woman, but she had opted out of her employer-sponsored health insurance because she couldn’t afford the premium. She’d occasionally had coverage in the past, but it never guaranteed that she’d actually be able to afford health care. She called me once, defeated, because she was trying to fill a prescription at Walgreens and the pharmacy had flagged an issue with her insurance. She would need to pay out of pocket, and she didn’t have the $134.89. She was often frustrated by spending long spells on hold with insurance agents, and was overwhelmed by the complexity of the plans.

[Annie Lowrey: Annoying people to death]

My aunt’s experience with the health-care system is familiar to many Americans. In a 2023 survey by the Kaiser Family Foundation, nearly a quarter of adults said signing up for a plan was simply too confusing. Even those who have coverage may decide to delay or skip treatment because they can’t afford the out-of-pocket costs, resulting in emergency-room visits and hospitalizations that could have been prevented.

Some years, my aunt made so little money that she might have qualified for Medicaid, but not recently—the income cutoff if you’re single in Kentucky is $1,835 a month. Some years, she bought coverage through the Affordable Care Act’s exchanges, but eventually she decided it was too expensive.

Many more people are now making that same decision. In 2025, the Republican-controlled Congress voted to let Biden-era subsidies in the ACA, which had helped some 22 million people afford their coverage, expire. Within just two weeks of the cutoff, at the end of December, enrollment had dropped by 1 million people. According to one group’s estimate, families are paying $200, $300, or $1,000 more a month; many have seen their premiums double.

[Read: The coming Obamacare cliff]

In January, President Trump released his proposal for a “Great Healthcare Plan,” which suggests that savings from the former subsidies could be sent directly to “eligible” Americans. But who would be eligible? The proposal makes no mention of the many people who don’t have coverage. Then, in February, the Trump administration released a list of 43 prescription drugs that Americans can buy for reduced prices. But some of these were already available at those prices or in generic forms, and they make up a tiny fraction of the drugs Americans need; the prescription my aunt couldn’t afford, for instance, is not listed.

Nothing about Trump’s pronouncements changes the fact that millions more Americans will soon be stuck where my aunt was: in the middle—sometimes insured, sometimes uninsured, but always too poor to get the care they need.

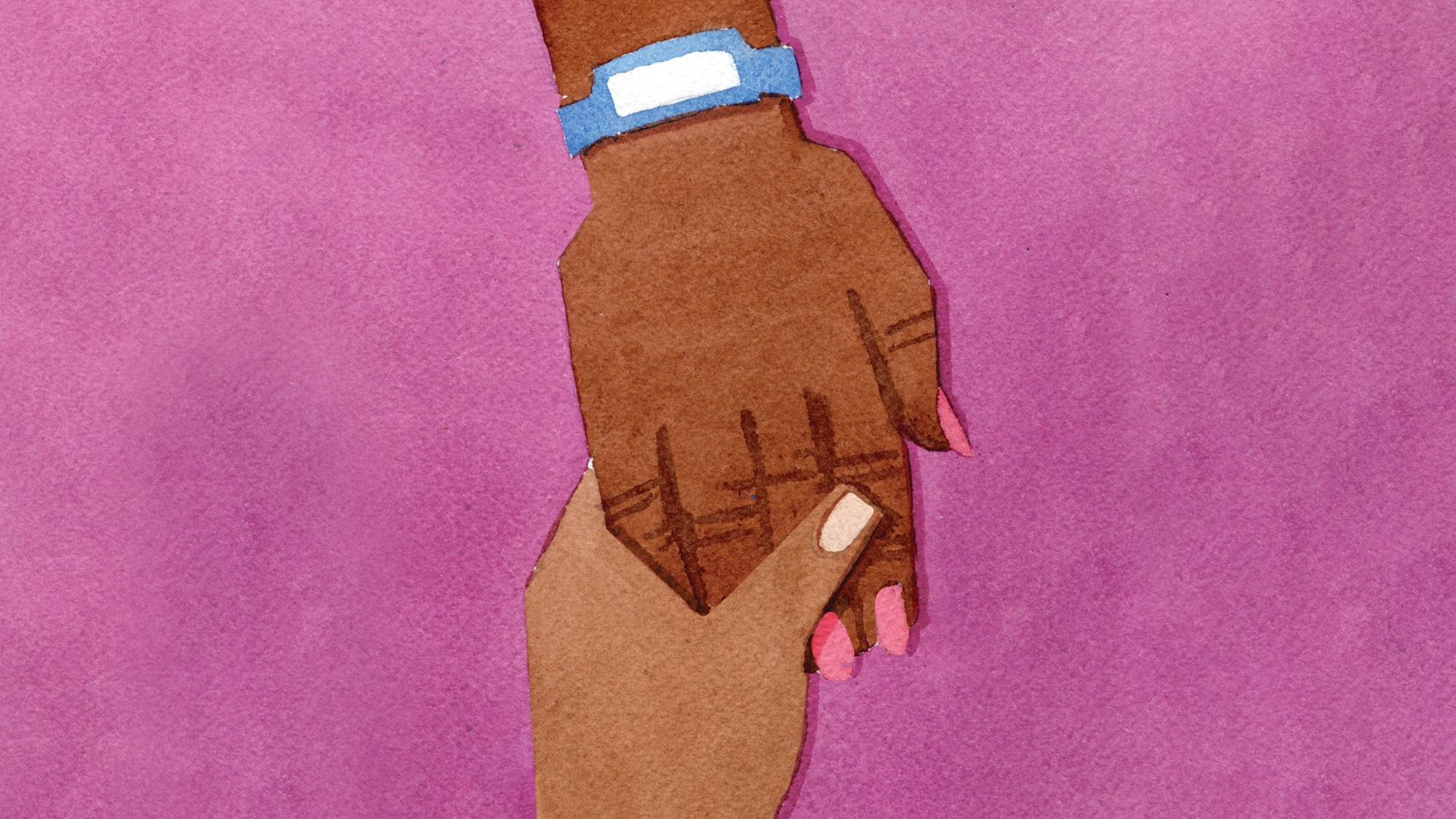

As I stared at my aunt in the ICU, I noticed that her eyebrows were freshly waxed, and her nails had bleach-white French tips. Only the week before, she’d texted me about getting her nails done. It was an indulgence she rarely allowed herself: “Woo this pedi feels good. I haven’t had one since last year.” When I rubbed Vaseline on her chapped feet, I discovered her ruby-red toenails.

She could not have known that the decision to finally splurge a little on herself would be a conversation starter with the nurses, who complimented her on her nails and eyebrows. Her grooming signaled to them that she was someone who took care of herself, someone who deserved their attention and respect.

I drove to her house later that week to meet her younger son. We’d planned to check on her bills—to see if we could find her bank PIN or account information to make sure that her finances stayed on track. I found notebooks coated with her handwriting, a list of numbers down each page that looked like an unsolved equation. These, I realized, were her monthly expenses, along with details such as the confirmation codes for bills she’d paid. Stuffed inside one notebook was a pawn-shop notice, announcing its full ownership over an item she’d traded in.

For years, not having enough money nibbled at my aunt’s health. She texted me about having severe pain in her back and breasts. She wrote that she had a “knot” in one breast—“I’m thinking just polyps.” She lost a lot of weight and said she was feeling depressed. I suggested reaching out to a psychiatrist to ask for antidepressants. She wrote back: “That cost. That’s why I need insurance.” She was tired of pretending to be okay. After paying for her mortgage, water bill, Wi‑Fi, car insurance, and other necessities each month, she’d usually be out of money. She was always transparent with me about her struggles, and sent photos of bills with disconnect notices: a letter from the energy company; an available checking balance of –$59.70; a past-due payment, with the amount owed in bold. Shutoffs have resumed. Make a $172.75 payment today to get your account back on track. She had small wins, such as finally paying off her car. But she still went back and forth to the payday-loan store.

As I sat next to her in the hospital, I couldn’t help but feel guilty. For years, I had been sending her money when she asked, but sometimes I didn’t. I would listen to her struggles and then go on with my life. I was grateful to be financially stable, but frustrated by being the financial rescuer for family members. I wanted to create boundaries, and to escape from the transactional, lopsided part of these relationships.

[From the October 2023 issue: Jenisha from Kentucky]

But I had not thought enough about how much she gave me—in every way she could. She posted about my accomplishments on Facebook no matter how small I considered them. She filled voids for me: self-esteem booster, cheerleader, second mother. In 2014, she used all the money she had to fly to New York to see me graduate from Columbia. She was the only member of my family there. When my name was called and I walked across the stage, she cried so much that someone had to hand her a tissue.

A few months ago, my son turned 4, and my aunt was determined to send him a gift. A manila envelope arrived at my apartment: She had mailed him five individually wrapped Hot Wheels cars and a Spider-Man birthday card. I recorded a video as my son stuffed his hand inside the envelope, pulling out each toy, saying, “Oh, wow. This is awesome.” That night, I sent the video to my aunt. She wrote back at 2 a.m.: “Up looking at videos over n over. He was so excited.” She was always trying to give to others, even though she never had enough for herself.

As individuals, and as a country, we tend to pay attention only when it’s too late. Americans who want to cut health-care spending don’t seem to understand that access to preventive care saves not just lives, but also money. Perhaps my aunt’s hospital stay could have been avoided if she’d been able to call a doctor and make an appointment, an option that so many of us take for granted. What is a life like my aunt’s worth in America? Unfortunately, that determination has been made.

[Jonathan Chait: Obamacare changed the politics of health care]

My aunt hasn’t sat up or spoken since the aneurysm, and no one knows if she will again. In January, she was transferred from the hospital to a nursing home. She’s supposed to go home soon, to be cared for by the family, who can’t possibly give her the round-the-clock care she needs. She’s not capable of worrying about health insurance at this point, but if she were, she wouldn’t have to: Now that she’s completely disabled, she qualifies for Medicaid.

This article appears in the April 2026 print edition with the headline “The Cost of Not Having Health Insurance.”